PPP + EIDL Eligibility for Foreign-Owned U.S. Businesses

Kegler Brown Global Business News April 21, 2020

Smart Summary

- U.S. companies with foreign ownership may be eligible for both the PPP and EIDL government loan programs, depending on corporate structuring.

- EIDL eligibility counts employees of all affiliated companies, whether U.S. or non-U.S., toward the general 500 cap.

- The PPP is more lenient, and counts employees of all affiliated companies toward the 500 general cap ONLY IF they have a principal place of residence in the U.S.

In light of the new loan programs from the Small Business Administration (“SBA”), small businesses all over the United States have acted quickly to apply for and obtain the newly available funds. Both the Paycheck Protection Program (“PPP”) and the Economic Injury Disaster Loans (“EIDLs”) provide a small business owner with operating capital necessary to implement a holistic cash access strategy in order to survive – and possibly thrive – during this “Great Pause.”

A savvy business owner can combine both the PPP and EIDLs to have many operating expenses entirely covered while weathering the storm of U.S. government-imposed lockdowns. This is very clear for companies based in the U.S., but what about U.S.-based businesses with foreign parent companies? Can they take advantage of the PPP and EIDL? The answer is: maybe.

A U.S.-based company owned by a foreign company may be eligible for both the PPP and an EIDL. In most of these cases, the answer will depend on two things: 1) number of employees, and 2) the organizational structure of the conglomerate.

Number of Employees Under EIDLs + the PPP

Although there are several eligibility requirements, an applicant business is generally eligible for a loan under either program if it has fewer than 500 employees. If a business has more employees, it may still be eligible if the size is considered “small” based on industry standards, as determined by the SBA. Under both programs, employees of affiliates are attributable to an applicant. However, to make matters more confusing, the number of employees attributable to an applicant are calculated differently under each program.

Number

of Employees under an EIDL – Foreign Affiliate Employees Count

A

U.S. company owned by a foreign company has at least one affiliate (its parent

company and possibly other companies also owned by the parent company). For

purposes of an EIDL, all employees of affiliates are

counted against an applicant, regardless of the employee’s principal place of

residence. If a company is found to be an affiliate of an applicant, then all

employees of the affiliate, both U.S. and non-U.S., are counted against the

applicant.

Number

of Employees under the PPP – Foreign Affiliate Employees Might Not Count

Unlike

the EIDL program, the PPP makes an important distinction with respect to employees

of affiliates. Based on guidance issued by the SBA, only employees of affiliates having a

principal place of residence in the United States count against an

applicant for purposes of determining eligibility under the PPP. Therefore,

even if a U.S. company with a foreign parent company and foreign affiliates

would be well over the 500 threshold for purposes of an EIDL, it may be

eligible for a PPP if, between the applicant and its affiliates, there are not

greater than 500 employees having a principal place of residence in the United

States.

Affiliation- Why Your Company Structure Matters

The structure of an applicant’s parent company will determine how many affiliates are attributable to an applicant. A comprehensive analysis of the SBA’s affiliation rules is necessary to conclusively determine whether entities are affiliates. But generally speaking, entities are affiliates if one controls the other or a third party has the power to control both. Control is determined by analyzing the governing documents of the entities. Notably, control may be found even if there is simply an ability to block action by the entity, or “negative control.”

Examples + Related Eligibility

As we mentioned above, the structure of the conglomerate matters for determining eligibility under the PPP and an EIDL. Here are examples some examples.

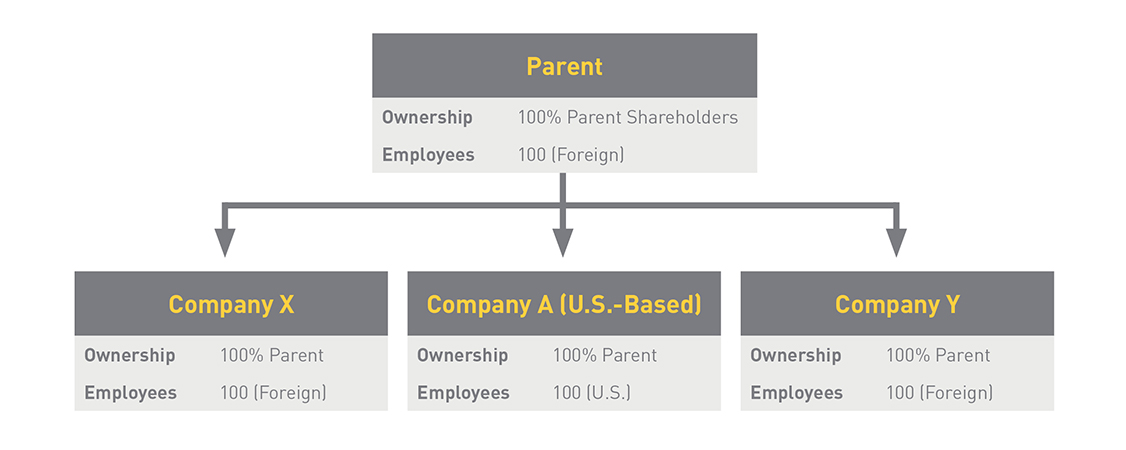

Company A – Eligible for PPP and EIDL

Result: Company 1 is eligible under the PPP and for an EIDL.

Explanation: Parent, Company X, and Company Y would be considered affiliates. Because Parent has the ability to control Company A (via its 100% ownership), Parent is an affiliate of Company A. Further, because Parent has the power to control Company A, Company X, and Company Y, they would also be considered affiliates. Therefore, for purposes of Company A’s eligibility under an EIDL, the total number of employees attributable to it would be 400. Company A is also eligible under the PPP because only 100 of the total employees have a principal place of residence in the U.S.

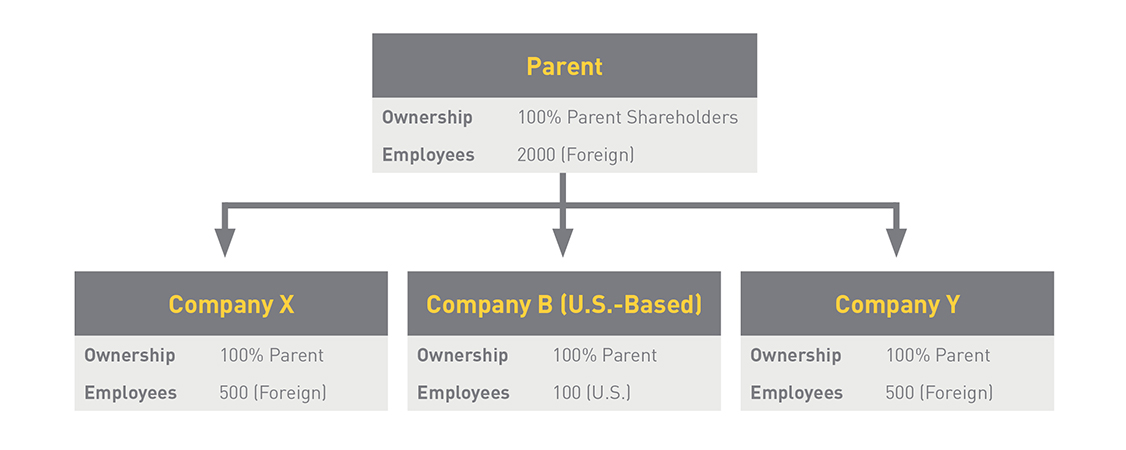

Company B – Eligible for PPP, but not EIDL

Result: Company B is eligible under the PPP, but not for an EIDL.

Explanation: Parent, Company X, and Company Y would be considered affiliates. Because Parent has the ability to control Company B (via its 100% ownership), Parent is an affiliate of Company B. Further, because Parent has the power to control Company B, Company X, and Company Y, they would also be considered affiliates. Therefore, for purposes of Company B’s eligibility under an EIDL, the total number of employees attributable to it would be 3,100. However, Company B is eligible under the PPP because only 100 of the total employees have a principal place of residence in the U.S.

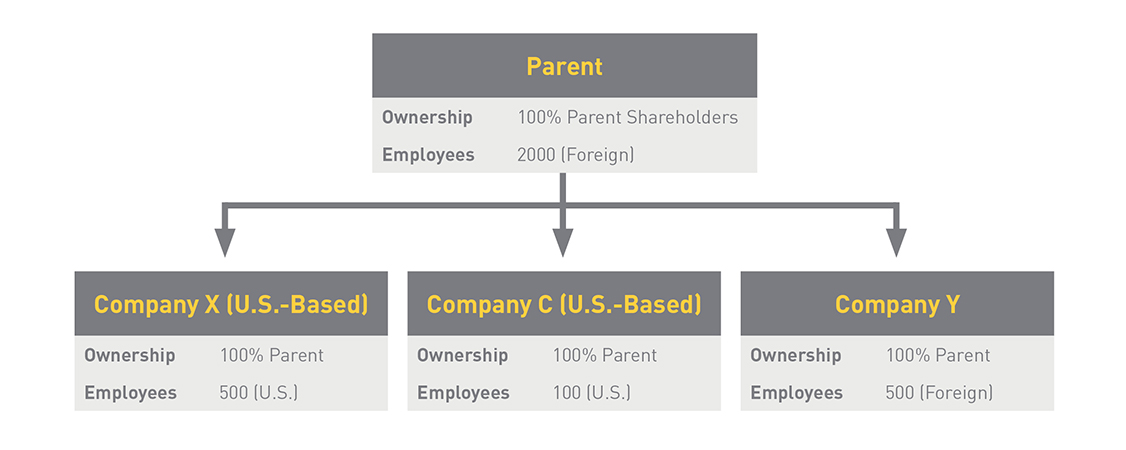

Company C – Not Eligible for the PPP or EIDL

Result: Company C is not eligible under the PPP or for an EIDL.

Explanation: Parent, Company X, and Company Y would be considered affiliates. Because Parent has the ability to control Company C (via its 100% ownership), Parent is an affiliate of Company C. Further, because Parent has the power to control Company C, Company X, and Company Y, they would be considered affiliates. Therefore, for purposes of Company C’s eligibility under an EIDL, the total number of employees attributable to it would be 3,100. Company C is also not eligible under the PPP because 600 of the total employees (Company C’s and Company X’s) have a principal place of residence in the U.S.

What You Should Do

If you are a U.S.-based company owned by a foreign company, you may be eligible under these loan programs. The answer lies in the total number of employees under your parent company’s corporate umbrella, how many of them would be attributable to you under the affiliation rules, and where the employees have a principal place of residence. You should contact legal counsel familiar with the SBA’s affiliation rules and both programs to make the ultimate decision as to your eligibility for an EIDL or under the PPP.

Cody Myers is a business attorney and is leading the firm’s team focused on helping companies apply for and manage their loan funds under the PPP and EIDL. He can be reached directly at [email protected] or (614) 462-5495.

Vinita Mehra is a director and chair of the firm’s Global Business team, working with U.S. subsidiaries of companies based outside the U.S. in coordinating, acquiring and maximizing federal loans as a result of the pandemic. She can be reached directly at [email protected] or (614) 255-5508.